What Is the Opening Range?

The opening range is the price range established during the first few minutes of a trading session. It's defined by the high and low of a specific time window after the market opens — typically the first 5, 15, or 30 minutes.

For NQ futures (Nasdaq-100 E-mini), the regular trading session opens at 9:30 AM Eastern. So a 15-minute opening range captures the high and low between 9:30 and 9:45 AM. That's it. Two numbers — a high and a low — that define the battlefield for the rest of the session.

The concept was popularized by Tony Crabel in his 1990 book "Day Trading With Short Term Price Patterns And Opening Range Breakout." The book became so influential (and so hoarded by institutional traders) that used copies now sell for hundreds of dollars. Crabel's thesis was straightforward: the opening range captures the initial equilibrium between buyers and sellers, and a breakout from that range signals a directional commitment worth trading.

The Three Common ORB Windows

- 5-Minute ORB: Captures the first 5 minutes (9:30–9:35 AM ET). Fastest signals, most false breakouts. Best suited for experienced scalpers who can handle the noise. The range is narrow, so you get more signals — but more of them are garbage.

- 15-Minute ORB: Captures 9:30–9:45 AM ET. The sweet spot for most NQ futures traders. Wide enough to filter out the open's initial chaos, narrow enough to offer reasonable risk/reward. This is the window most backtests focus on.

- 30-Minute ORB: Captures 9:30–10:00 AM ET. More reliable but produces fewer trades. The wider range means larger stop distances, which requires bigger accounts or smaller position sizes. Better for swing-style intraday trading.

Each window has tradeoffs. The narrower the window, the more signals you get — and the more of those signals will be false breakouts that reverse immediately. The wider the window, the more reliable the breakout — but your risk per trade increases proportionally.

Why NQ Specifically?

NQ futures are uniquely suited to ORB because of their volatility profile. NQ typically moves 1.5-2x the daily range of ES. That means the opening range produces wider price swings, larger breakout moves, and more potential profit per trade. But it also means more violent fakeouts. You can't trade NQ like you trade ES — the volatility demands tighter discipline and better filters.

How ORB Works for NQ Futures: Entry & Exit Rules

The basic ORB setup is deceptively simple. That simplicity is both its appeal and its trap — because "simple" doesn't mean "easy to profit from."

The Classic ORB Rules

Step-by-Step Setup

- Mark the opening range: After your chosen window closes (e.g., 9:45 AM for 15-min ORB), record the high and low of that period.

- Wait for a breakout: Enter long when price breaks above the opening range high. Enter short when price breaks below the opening range low.

- Place your stop: The opposite side of the opening range. If you went long above the high, your stop sits at or below the opening range low (or a fraction of the range — more on the 25% rule later).

- Set a target: Common targets include 1x the opening range width (1R), 1.5x, or 2x. Some traders use the prior day's range or ATR-based targets instead.

- Time cutoff: Close all ORB trades by a fixed time — typically 2:00 PM or 3:00 PM ET. ORB is a momentum play, and if it hasn't worked by mid-afternoon, it's not going to.

Concrete Example: 15-Minute ORB on NQ

---

15-min Opening Range (9:30–9:45):

High: 21,450

Low: 21,380

Range width: 70 points ($1,400/contract)

---

10:02 AM: Price breaks above 21,450

→ Long entry at 21,451

→ Stop at 21,380 (70 pts risk = $1,400)

→ Target at 21,520 (1R = 70 pts = $1,400)

→ Extended target at 21,555 (1.5R = $2,100)

That's $1,400 risk for $1,400–$2,100 reward per contract. On a 1-lot, the math works if your win rate is above 50% at 1R or above 40% at 1.5R. The problem is that raw ORB win rates on NQ have been falling over the last decade. Which brings us to the uncomfortable truth.

The Backtest Reality Check

Here's where most ORB content on the internet stops being honest. They show you the setup, maybe a handful of cherry-picked winning trades, and tell you to "be disciplined." Let's look at what the data actually says.

The Good: ORB Has Historical Merit

When Crabel published his research in 1990, ORB was a genuine edge. The logic is sound: the opening range captures overnight sentiment meeting intraday liquidity. A breakout from that range, especially on volume, signals that one side has committed.

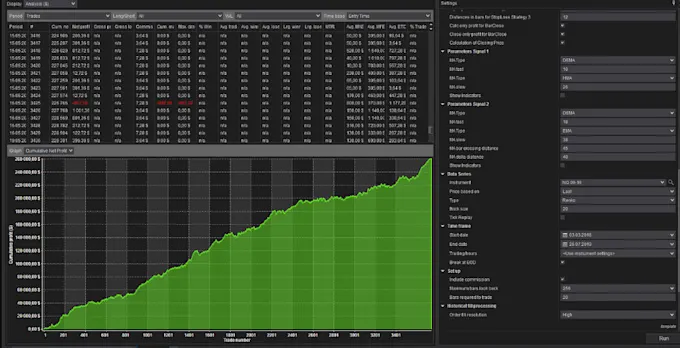

Various backtests have been published showing promising results. One widely-shared YouTube backtest showed a 56% win rate over 365 trading days on NQ, generating roughly $103K in profit. A Reddit community backtest tracked approximately 900 trades on MNQ from 2019 to 2026 using a 15-minute ORB. These numbers look attractive.

The Bad: The Edge Has Eroded

Here's what those YouTube thumbnails don't tell you: raw, unfiltered ORB doesn't work like it used to.

Research from QuantifiedStrategies.com found that raw ORB applied to the S&P 500 no longer yields consistent profits. The strategy that worked beautifully in the 1990s and early 2000s has been gradually arbitraged away. Too many traders learned about it. Too many algorithms now front-run the breakout levels. The opening range high and low are the most obvious levels on every NQ chart every morning — which means they're also the levels most likely to be faded by institutional algos looking to trap breakout traders.

Why Raw ORB Underperforms in 2026

- Algo saturation: Every HFT firm and retail algo marks the opening range. Those levels are now magnets for stop hunts and liquidity grabs.

- False breakout frequency: Price routinely pokes above the OR high or below the OR low, triggers a wave of breakout entries, then reverses. This "breakout trap" pattern has become the dominant move on many sessions.

- Changed market structure: The rise of 0DTE options, Globex session volume, and pre-market news events means the "clean" opening that Crabel studied barely exists anymore.

- Crowded trade: ORB is massively popular in prop firm challenges (Apex, TopStep, etc.) because of its defined risk. That means thousands of traders are all entering at the same levels — creating perfect liquidity pools for larger players to fade.

The Honest Take

ORB isn't dead. The core concept — that a breakout from the opening range signals directional intent — is still valid market microstructure. But you need filters. You need context. You need to know when to trade the breakout and when to sit on your hands. Raw ORB applied blindly every morning will grind your account down with death-by-a-thousand-fakeouts.

The traders who are actually making money with ORB in 2026 are not the ones who mark two lines and hit buy. They're the ones who combine ORB with overnight context, volume confirmation, volatility filters, and regime awareness. Let's talk about those filters.

Key Filters That Actually Improve ORB

Every one of these filters has the same goal: eliminate the low-conviction breakouts and only trade the ones with genuine institutional momentum behind them.

1. Overnight Range Context

The Globex session (6:00 PM – 9:30 AM ET) creates its own price range before the cash session even opens. This overnight range is critical context that most ORB traders completely ignore.

- Narrow overnight range + wide opening range: High-conviction setup. Price consolidated overnight and is now expanding. Breakouts from this combination tend to follow through.

- Wide overnight range + narrow opening range: The move already happened. The breakout from a narrow opening range after a wide overnight range is often just noise — the real displacement occurred during Globex.

- Opening range inside overnight range: Price hasn't broken the overnight structure. Be cautious — the breakout needs to also clear overnight high/low to have real momentum.

- Opening range outside overnight range: The cash session immediately extended the overnight range. This is a strong signal of continuation — especially if the opening range breakout aligns with the overnight breakout direction.

2. Volume Confirmation

Volume doesn't lie. A breakout on expanding volume is institutional money committing to a direction. A breakout on thin volume is retail chasing — and institutional algos are about to fade it.

The filter: only trade ORB when the breakout bar's volume exceeds the average volume of bars within the opening range by at least 1.5x. If the breakout happens on weak volume, stand aside. The false breakout rate drops significantly when you add this single filter.

3. ATR-Based Volatility Filters

Not every day is an ORB day. On low-volatility, grinding sessions, the opening range will be tiny and every breakout will reverse. On extremely volatile days (FOMC, CPI, earnings bombs), the opening range will be so wide that your risk per trade becomes unmanageable.

The Volatility Sweet Spot

- Calculate the 14-day ATR on the NQ daily chart

- Calculate the opening range width as a percentage of ATR

- Skip the trade if the opening range is less than 15% of the 14-day ATR — range is too narrow, fakeouts likely

- Skip the trade if the opening range is more than 50% of the 14-day ATR — range is too wide, risk/reward is poor

- The sweet spot: opening range between 20-40% of the daily ATR

4. Trend Alignment (Higher Timeframe)

ORB in the direction of the prevailing trend has a materially higher win rate than counter-trend ORB. This should be obvious, but traders routinely ignore it.

The filter: check NQ's position relative to the 20-period EMA on the daily chart. If NQ is above the daily 20 EMA, only take long ORB breakouts. If NQ is below the daily 20 EMA, only take short ORB breakouts. This single filter eliminates roughly half of all ORB trades — and the half it eliminates is predominantly the losing trades.

5. Day-of-Week and Time-of-Day

Backtests consistently show that ORB performance varies by day of week. Mondays and Fridays tend to produce lower-quality breakouts — Mondays because of weekend gap dynamics, Fridays because of position squaring ahead of the weekend. Tuesday through Thursday tends to produce the cleanest ORB signals.

As for time of day: if the breakout hasn't occurred by 10:30 AM ET, the probability of a meaningful trend day drops sharply. The best ORB trades happen in the first 30-60 minutes after the opening range closes.

Automate Your Breakout Strategies

Our professional NinjaTrader strategies handle regime detection, entry filters, and risk management automatically. No more manually marking opening ranges at 9:30 AM.

The 25% Rule: Cut Losers Immediately

This is one of the most practical insights to come out of ORB research, and it's been validated by traders across different communities: if a breakout trade goes more than 25% of the opening range against you, kill it immediately.

The logic is rooted in market microstructure. A genuine breakout — one backed by institutional order flow — should show immediate displacement. Price should break the level and not look back. If it breaks out and then retraces 25% of the range, the breakout has failed. The institutional commitment isn't there. Holding and hoping only exposes you to a full reversal.

---

OR High: 21,450 | OR Low: 21,380

Range width: 70 points

25% of range: 17.5 points

---

Long entry at 21,451 (break above OR high)

25% stop: 21,433.5 (entry minus 17.5 pts)

---

If price hits 21,433.5 → EXIT. Don't wait for the full stop at 21,380.

Risk reduced from 70 pts ($1,400) to 17.5 pts ($350)

This dramatically changes your risk math. Instead of risking 70 points per trade, you're risking 17.5. Yes, you'll get stopped out more often — but the trades where you would've taken the full 70-point loss were almost never going to come back anyway. The 25% rule lets you take more shots with less capital at risk per attempt.

Important Caveat

The 25% rule works best on the 15-minute and 30-minute ORB. On the 5-minute ORB, the range is often so narrow that a 25% retracement can happen from normal bid/ask bounce. Adjust accordingly — some traders use 30-35% for the 5-minute window.

How to Automate ORB in NinjaTrader 8

NinjaTrader 8 is well-suited for ORB automation. The platform's session management tools and NinjaScript API give you everything you need to define the opening range, detect breakouts, and execute entries with proper risk management — all without watching the screen.

Session Templates: Define Your Opening Range Window

The first step is configuring NinjaTrader to recognize your opening range period. You can define a custom session template that isolates the first 15 (or 5 or 30) minutes of the regular session:

- Go to Tools → Session Manager in NinjaTrader 8

- Create a custom session template that defines the RTH (Regular Trading Hours) start time

- Your strategy will use this session definition to know exactly when the opening range begins

- In NinjaScript, the

SessionIteratorclass gives you programmatic access to session start/end times

Key NinjaScript Methods for ORB

Here are the core NinjaScript components you'll use to build an ORB strategy:

OnBarUpdate()— Your main logic method. On each bar close during the opening range window, track the running high and low. After the window closes, monitor for breakouts.SessionIterator— Use this to determine the current session's start time and programmatically calculate when the opening range window ends. Essential for handling overnight sessions and partial holidays correctly.Bars.IsFirstBarOfSession— Detects the first bar of a new session so you can reset your opening range variables. Without this, you'd carry stale levels from the previous day.EnterLongLimit() / EnterShortLimit()— Enter breakout trades. You can also useEnterLongStopMarket()to place stop orders at the opening range high/low for automatic breakout entry.SetStopLoss() / SetProfitTarget()— Define your risk management parameters. Set these dynamically based on the opening range width rather than using fixed point values.

Strategy Builder vs. Custom NinjaScript

NinjaTrader's Strategy Builder provides a no-code way to create basic ORB strategies using conditions and actions. You can define time-based conditions ("if time is between 9:30 and 9:45, track high/low") and breakout entries.

However, for a production-quality ORB strategy with all the filters we've discussed — volume confirmation, ATR filters, overnight range context, the 25% rule — you'll need custom NinjaScript. The Strategy Builder simply doesn't have the flexibility for multi-condition filtering and dynamic stop management.

NinjaScript ORB Logic Skeleton

// OnBarUpdate()

if (IsFirstBarOfSession)

ResetORBLevels();

if (IsWithinORBWindow())

TrackHighAndLow();

if (ORBWindowClosed && !HasEnteredToday)

{

if (PassesVolumeFilter() && PassesATRFilter()

&& PassesTrendFilter())

{

if (Close[0] > ORBHigh)

EnterLong();

if (Close[0] < ORBLow)

EnterShort();

}

}

// Apply 25% rule for active positions

if (Position.MarketPosition != MarketPosition.Flat)

Apply25PercentRule();

This is conceptual pseudocode to illustrate the logical flow. A production strategy would need proper state management, error handling, partial fill logic, and extensive backtesting.

Automation Pitfalls to Watch For

Automating ORB introduces its own set of problems that manual traders don't face:

- Slippage at breakout levels: Thousands of traders have orders stacked at the opening range high/low. Your fill may be 2-4 ticks worse than your intended entry. Account for this in backtests by adding realistic slippage.

- Session template misconfiguration: If your session template doesn't match the exchange's actual hours, your opening range will be wrong. Double-check against the CME's official NQ session times.

- Holiday/early close handling: Shortened sessions have different volatility profiles. Your strategy needs logic to detect and skip these days.

- Data feed gaps: If your data feed drops during the opening range window, your recorded high/low will be wrong. Build in data validation checks.

Risk Management for ORB on NQ

Risk management is where ORB strategies succeed or fail. The setup is simple — the risk control is what separates professionals from blowups.

Stop Placement Options

Full Range Stop

Stop at the opposite side of the opening range. Maximum risk, fewest premature stops. Works best with the 30-min ORB where ranges are wider and breakouts more reliable.

25% Rule Stop

Stop at 25% of the opening range from entry. Dramatically reduces risk per trade. Higher stop-out rate, but much better risk-adjusted returns over a large sample.

Midpoint Stop

Stop at the midpoint of the opening range. A compromise between the full range and 25% approaches. Popular with traders who find the 25% rule too aggressive.

ATR-Based Stop

Stop at a fixed ATR multiple (e.g., 0.5x daily ATR) regardless of opening range width. Normalizes risk across different volatility environments. More complex but more adaptive.

Position Sizing

NQ's $20/point contract value means even small opening ranges can produce significant dollar risk. The sizing rule is straightforward:

Fixed Fractional Sizing for ORB

---

$100K account, 1% risk = $1,000 max

Opening range = 50 pts = $1,000/contract

→ Trade 1 NQ contract (full range stop)

---

With 25% rule: risk = 12.5 pts = $250/contract

→ Could trade up to 4 NQ contracts at same risk

Never let the opening range width determine your size after the fact. Calculate your maximum position size before the session opens based on your account size and the prior day's ATR as a range estimate. If the actual opening range is wider than expected, reduce size — don't expand your risk budget.

Max Daily Loss Rules

ORB typically gives you one or two setups per day. If both fail, you're done. There's no "third try" that somehow works out.

Non-Negotiable Daily Limits

- Max 2 ORB trades per day. One in each direction, or two in the same direction if the first was stopped out cleanly and conditions are still valid.

- Max daily loss = 2-3% of account. If you hit this, close the platform. No revenge trading, no "one more try."

- Max consecutive losing days = 3. Three straight losing days means something has changed in the market regime. Stop, reassess your filters, review whether ORB is still appropriate for current conditions.

Common Mistakes That Kill ORB Traders

After years of watching traders blow up with ORB strategies, the same mistakes keep appearing. Every single one is avoidable.

Mistake #1: Trading Every Breakout Blindly

This is the #1 killer. Trader marks the opening range, price breaks above the high, they go long. Every. Single. Day. No filters, no context, no awareness of whether today is a trend day or a chop day.

Studies suggest that only 30-40% of trading days are genuine trend days where breakout strategies thrive. On the other 60-70%, the breakout will reverse and trap you. If you're not filtering for conditions that favor follow-through, you're gambling with worse-than-coin-flip odds and paying commissions for the privilege.

Mistake #2: Ignoring Overnight/Globex Context

NQ trades nearly 24 hours. By the time the 9:30 AM open arrives, significant levels have already been established during the Globex session. Ignoring the overnight high, overnight low, and the size of the overnight range is like walking into a poker game without looking at your cards.

If NQ gapped up 100 points overnight and the opening range high is already deep into overhead resistance, that "breakout" above the OR high is more likely to be the final push before a reversal. Context matters.

Mistake #3: No Regime Awareness

ORB performs very differently across market regimes. In a strong trending market, breakouts follow through beautifully. In a choppy, mean-reverting market, breakouts fail relentlessly. In a volatility expansion (like around FOMC), the opening range is too wide to trade effectively.

If you don't know what regime you're in, you don't know whether ORB is appropriate today. Period.

Mistake #4: Curve-Fitting Backtest Parameters

"I tested every combination of opening range window, stop distance, target multiple, day-of-week filter, and time filter. I found the perfect combination that returned 400% over 3 years."

No, you found a curve-fit. If your backtest has more than 3-4 optimizable parameters, you're almost certainly fitting to noise. The more parameters you optimize, the more you're describing the past rather than predicting the future. A robust ORB strategy should work with reasonable parameters across multiple years and market regimes — not just the specific combination that happened to work on your test period.

For more on avoiding backtesting traps, see our comprehensive backtesting guide.

Mistake #5: Using ORB for Prop Firm Challenges Without Understanding Why

ORB has become the go-to strategy for prop firm challenges (Apex, TopStep, etc.) because of its defined risk. The reasoning: "I know exactly how much I can lose per trade." That's good risk management. But here's the problem — traders optimize their ORB specifically to pass the challenge rules (max drawdown, profit target, trading days required), not to make money in live markets.

A strategy tuned to pass a prop firm eval on MNQ with exactly the right parameters will often fail when you scale to NQ on a funded account. The market doesn't care about your evaluation rules.

The Bottom Line

Opening Range Breakout is a legitimate strategy with real market microstructure behind it. The idea that the opening range captures the initial balance between buyers and sellers, and that a breakout signals a directional commitment — that's sound logic. It worked for Crabel in 1990, and the core concept still works in 2026.

What doesn't work anymore is raw, unfiltered ORB applied blindly every session. The edge has eroded because every retail trader and their algo knows where the opening range high and low are. Those levels are now liquidity traps as often as they are genuine breakout zones.

The traders making money with ORB in 2026 are doing it with layers of context: overnight range analysis, volume confirmation, ATR-based volatility filters, trend alignment, and the 25% rule for cutting failed breakouts immediately. They're not trading every day. They're selective. They understand that ORB is a sometimes strategy, not an always strategy.

If you want to add ORB to your NQ playbook, start with the 15-minute window, add two or three filters, and backtest across at least 3 years of data with realistic slippage and commissions. If the results look too good, you've probably curve-fit. If they look modestly profitable with manageable drawdowns, you might have something worth trading live — at minimum size — to see if the results hold.

That's the boring, honest answer. It won't get a million views on YouTube. But it's the approach that actually keeps your account alive.