What Mean Reversion Actually Is (And Isn't)

Mean reversion is the observation that price tends to return to an average value after deviating from it. That's it. Not a guarantee. Not a law. An observation with statistical tendencies that hold under specific conditions and completely fall apart under others.

The concept has deep roots in statistics — Francis Galton described "regression toward the mean" in the 1880s studying hereditary traits. In markets, it means that when NQ trades significantly above or below a meaningful average (like VWAP or a moving average), there's a tendency for price to revert back toward that level. The tendency is real. The problem is that traders treat it like a certainty.

The "Buy Every Dip" Myth

Let's kill this immediately. Mean reversion is not "buy every dip." It's not "price dropped 50 points so it must bounce." It's not "RSI hit 30 so I'm going long." Every one of those can be true in a range-bound market and catastrophically wrong in a trending one. The trader who buys every dip in a grinding downtrend doesn't practice mean reversion — they practice account destruction. Mean reversion requires overextension relative to a defined average, confirmation that momentum is exhausting, and a market regime that supports reversion. Without all three, you're just guessing with a fancy name.

The Statistical Foundation

In a normally distributed system, roughly 68% of observations fall within one standard deviation of the mean, and 95% fall within two. Markets aren't perfectly normally distributed — they have fat tails and skew — but intraday NQ price action around VWAP approximates this closely enough to be useful. When price moves 2+ standard deviations from VWAP, the probability of reverting toward the mean increases. Not to 100%. Not even to 80%. But enough to create a statistical edge when combined with the right filters.

The key phrase there is "when combined with the right filters." Raw mean reversion — blindly fading every extension — has a win rate around 55-60% in range-bound conditions and somewhere near 25-30% when a trend is in effect. That second number will obliterate your account faster than you think, because the losses in trending markets are often multiples of your typical winning trades.

Key Levels That Act as Magnets

Mean reversion trades need a "mean" to revert to. Not all averages are equal. Here are the levels that consistently act as price magnets on NQ futures, ranked by intraday reliability.

1. VWAP (Volume-Weighted Average Price)

VWAP is the gold standard for intraday mean reversion. It represents the average price weighted by volume — in other words, where the majority of contracts actually traded. Institutional algorithms use VWAP as a benchmark for order execution, which creates a self-reinforcing magnet effect: large orders push price toward VWAP, and when price deviates significantly, those same algos treat the deviation as an opportunity.

On NQ, VWAP reversion trades work best during the midday session (11:00 AM – 2:00 PM ET) when directional momentum has faded and institutional algorithms are filling orders. The morning session (9:30–11:00) is dominated by momentum and news flow, making VWAP fades dangerous. The key is knowing when VWAP acts as a magnet and when it's just a line that price is ignoring.

2. Prior Day Close (Settlement)

The prior day's settlement price is one of the most underrated levels in futures trading. It represents where the market found equilibrium at the end of the previous session. When NQ opens above or below this level, there's a measurable tendency to retest it during the first few hours of trading — particularly when the gap is less than 0.5% of price.

Gaps above 0.5% are more likely to represent genuine overnight re-pricing (news, earnings, macro events) and less likely to fill quickly. Small gaps, however, are often noise — and the prior day close acts as a gravity well that pulls price back.

3. Overnight Midpoint

The midpoint of the Globex session range (overnight high + overnight low, divided by two) represents the equilibrium of pre-market trading. It's not as widely tracked as VWAP, which is precisely why it still works. When price deviates significantly from the overnight midpoint during the RTH session, there's a reversion tendency — especially on days when the overnight range was relatively narrow (suggesting consolidation rather than a directional move).

4. Weekly VWAP

Weekly VWAP is the institutional timeframe for mean reversion. While daily VWAP resets each session, weekly VWAP carries across the entire trading week, providing a broader view of where the "fair value" sits. Significant deviations from weekly VWAP (2+ standard deviations on the weekly bands) often set up multi-day reversion trades. This is more of a swing-trading level, but intraday traders should be aware of it as context: if NQ is 200+ points above weekly VWAP, the intraday bias for mean reversion trades shifts toward the short side.

Quick Reference: Level Priority for Intraday Mean Reversion

- Primary target: Daily VWAP — most reliable intraday magnet

- Secondary target: Prior day close — especially for gap-fill trades

- Context level: Overnight midpoint — best when overnight range was narrow

- Macro context: Weekly VWAP — directional bias for the week

Entry Criteria: Overextension Filters

Finding a mean to revert to is step one. Step two is confirming that price is actually overextended — not just moving away from the average in a directional market. Here are the filters that separate a genuine mean reversion setup from a bad fade.

2σ Bollinger Bands

Bollinger Bands set at 2 standard deviations around a 20-period moving average provide a visual and quantitative measure of overextension. When price touches or exceeds the outer band, it's statistically in the top/bottom 5% of recent price distribution. That's your overextension signal.

But here's the trap: in a strong trend, price can ride the upper Bollinger Band for hours. The band touch is a necessary condition, not a sufficient one. You need the band touch plus a sign that momentum is actually exhausting. A band touch during a parabolic move up is not a short signal — it's a "stand aside" signal.

RSI Extremes

RSI (Relative Strength Index) on a 14-period setting provides momentum context. For NQ mean reversion:

- RSI above 75 on a 5-minute chart: Potential short-side mean reversion setup. Price is overbought on a short-term basis.

- RSI below 25 on a 5-minute chart: Potential long-side mean reversion setup. Price is oversold on a short-term basis.

- RSI divergence: Price makes a new high but RSI makes a lower high (or vice versa). This is the strongest signal — it indicates that momentum is waning even as price continues to extend. RSI divergence combined with a Bollinger Band touch is a high-conviction setup.

Don't use the default RSI levels of 70/30. On NQ intraday charts, those levels trigger too frequently during normal price movement. Pushing to 75/25 or even 80/20 on 5-minute charts reduces noise significantly and isolates genuinely overextended conditions.

Delta Divergence

Cumulative delta — the running total of volume traded at the ask minus volume traded at the bid — reveals whether buyers or sellers are actually aggressive. Delta divergence occurs when price makes a new extreme but cumulative delta doesn't confirm it.

Example: NQ prints a new session high, but cumulative delta is flat or declining. This means the new high is being driven by passive buying (limit orders being absorbed) rather than aggressive buying (market orders hitting the ask). Passive-driven highs are far more likely to revert than aggressive-driven ones. If you have access to order flow tools in NinjaTrader, delta divergence is arguably the single best confirmation filter for mean reversion entries.

The Triple Confirmation Setup

The highest-conviction mean reversion entries combine all three:

- Price at or beyond the 2σ Bollinger Band

- RSI at 75+ (for shorts) or 25- (for longs), ideally with divergence

- Delta divergence showing exhaustion of aggressive flow

This combination occurs maybe 2-4 times per week on NQ. That's not a lot of trades. But the win rate on this setup in a range-bound environment is significantly higher than any single-condition entry.

The Critical Difference: Trending vs. Ranging Markets

This is the section that determines whether mean reversion makes you money or blows you up. Mean reversion only works in ranging (rotational) markets. In trending markets, it's a wealth transfer mechanism — from your account to the traders on the other side of your fade.

Why Regime Matters More Than Entry

You can have the perfect mean reversion entry — RSI divergence, Bollinger Band touch, delta exhaustion — and still lose catastrophically if you're fading a genuine trend. On trend days, "overextended" is meaningless. NQ can move 300+ points in one direction, touching the 2σ band repeatedly, with each touch looking like a reversal setup and each one failing.

Research suggests that roughly 15-20% of trading days are genuine trend days on NQ. On those days, the market moves directionally from open to close with minimal retracement. Mean reversion on a trend day is like standing in front of a freight train because it "has to slow down eventually." It does. Eventually. After running over your stop loss.

How to Detect the Regime

There's no single indicator that perfectly identifies market regime. But several approaches, used together, get you close enough to be useful:

- ADX (Average Directional Index): ADX above 25-30 on a 15-minute chart signals a trending environment. ADX below 20 signals a range-bound market. The problem: ADX is a lagging indicator. By the time it crosses 30, you've already been fading the trend for an hour. Use it as context, not as a real-time trigger.

- Bollinger Band Width: When the bands are expanding rapidly, the market is trending. When they're contracting, it's ranging. Band width percentile (current width relative to the last 100 periods) is more useful than raw width. If band width is above the 80th percentile, trending conditions are likely — skip mean reversion trades.

- VWAP Slope: A steeply sloping VWAP indicates strong directional flow. When VWAP is essentially flat (slope near zero), rotational conditions favor mean reversion. This is one of the simplest and most practical regime filters.

- Opening 30-Minute Range vs. ATR: If the first 30 minutes of trading produce a range greater than 40% of the 14-day ATR, the session is likely to be a trend day. This early signal gives you the most actionable warning to avoid mean reversion trades.

- Volume Profile Shape: A balanced (bell-shaped) volume profile indicates rotation. A skewed or elongated profile with single prints indicates trend. If you're using Market Profile or volume profile tools in NinjaTrader, the shape of the developing profile is one of the best real-time regime indicators available.

The Simple Rule

If price has been on one side of VWAP for the entire session and VWAP is sloping noticeably, it's a trend day. Do not fade it. If price has crossed VWAP 3+ times and VWAP is relatively flat, it's a rotation day. That's your playground. This isn't sophisticated, but it's more effective than most complex regime detection schemes.

Stop Placement: Why Most Retail Traders Get Wrecked

Mean reversion stops are uniquely dangerous because the trade thesis is "price has gone too far." But how do you define "too far" when you're already fading an extreme? If price has moved to the 2σ band and you're fading it, where does your stop go? At the 3σ band? What if it goes to 4σ? In a genuine trend, standard deviation levels are meaningless — the distribution itself is shifting.

The Retail Trap: No Stop or Wide Stop

Most retail traders who lose money with mean reversion fall into one of two traps:

- No stop — "it has to come back": Famous last words. NQ can move 400 points in a single session. Without a stop, one trend day can wipe out weeks of successful mean reversion trades. This is the #1 cause of catastrophic losses in mean reversion strategies.

- Stop too wide — "giving it room to work": A 100-point stop on a mean reversion trade targeting 20 points of profit is 5:1 negative risk/reward. Even with a 90% win rate, you'd barely break even. The math doesn't work at scale.

Practical Stop Approaches

ATR-Based Stop

Use 1.5x the ATR of the timeframe you're trading. On a 5-minute NQ chart with a 5-period ATR of 15 points, your stop is 22.5 points from entry. This adapts to current volatility — wider in volatile conditions, tighter in calm ones.

Structure-Based Stop

Place the stop beyond the nearest structural level — a prior swing high/low, the 3σ Bollinger Band, or the overnight high/low. If price breaks that structure, the mean reversion thesis is invalid and you should be out.

Time-Based Stop

If the reversion hasn't started within 10-15 minutes of entry, exit at market. Genuine mean reversion moves tend to start relatively quickly. A trade that just sits at the extreme without reverting is likely in a trending environment where your filters failed.

Dollar-Based Stop

Define your maximum loss per trade in dollars, not points. On NQ ($20/point), a $500 risk budget means a 25-point stop. Simple, account-appropriate, and impossible to rationalize away. This forces you to size correctly from the start.

The best approach combines a structural stop with a time stop. Enter when your conditions align, set a hard stop at the nearest structural level, and if the trade hasn't started working within 10-15 minutes, exit regardless. Most winning mean reversion trades show immediate movement toward the mean. If it's not happening, the regime is wrong and you need to get out before the trend confirms.

Automate Your Mean Reversion Setups

Our NinjaTrader strategies include built-in regime detection and mean reversion logic — so you only fade when the conditions actually support it.

NinjaTrader 8 Implementation

NinjaTrader 8 has native support for most of the indicators used in mean reversion strategies. Here's how to build a functional mean reversion workspace and the NinjaScript logic for automation.

The Indicator Stack

Set up a chart template with the following indicators. Each one serves a specific role in the mean reversion decision process:

- VWAP (built-in): Add from Indicators → Order Flow → VWAP. This is your primary reversion target. Enable the standard deviation bands (±1σ and ±2σ) directly in the VWAP indicator settings.

- Bollinger Bands (built-in): 20-period, 2 standard deviations on the 5-minute chart. Use as your overextension filter. When price hits the outer band AND is beyond VWAP ±2σ, you have double confirmation of overextension.

- RSI (built-in): 14-period on the 5-minute chart. Customize the overbought/oversold levels to 75/25 instead of the default 70/30. Display in a separate panel below the chart.

- ADX (built-in): 14-period on the 15-minute chart. Use for regime detection — above 25 means trending conditions, below 20 means ranging. You may want this on a separate 15-minute chart rather than the 5-minute execution chart.

- Order Flow Cumulative Delta (built-in): Available in NinjaTrader's Order Flow+ suite. Display cumulative delta as a histogram below price to visually identify delta divergence at price extremes.

NinjaScript Strategy Logic

Here's the conceptual logic for automating a mean reversion strategy in NinjaScript:

Mean Reversion Logic Skeleton

// OnBarUpdate()

// Step 1: Regime Check

bool isRanging = ADX(14)[0] < 22

&& VWAPSlope is near flat;

if (!isRanging) return; // No trades in trends

// Step 2: Overextension Check (Long Side)

bool oversold = Close[0] <= BollingerLower(2, 20)[0]

&& RSI(14)[0] < 25;

// Step 3: Momentum Exhaustion

bool deltaDiv = Close[0] < Close[1]

&& CumulativeDelta[0] > CumulativeDelta[1];

// Step 4: Entry with defined risk

if (oversold && deltaDiv && TimeConditions())

{

EnterLong();

SetStopLoss(CalculationMode.Ticks, atrStop);

SetProfitTarget(VWAP distance);

}

// Time-based exit: close if no reversion in 15 min

if (BarsSinceEntry() > timeLimitBars)

ExitLong();

This is conceptual pseudocode illustrating the decision flow. Production code requires proper state management, multi-timeframe data series for ADX, and robust error handling. See our backtesting guide for testing methodology.

Multi-Timeframe Setup in NinjaTrader

Mean reversion strategies typically require at least two timeframes: an execution timeframe (5-minute) and a context timeframe (15 or 30-minute). In NinjaTrader 8, you handle this with AddDataSeries() in the OnStateChange() method:

- Primary series (BarsInProgress == 0): 5-minute NQ chart for entry execution, RSI, and Bollinger Bands

- Secondary series (BarsInProgress == 1): 15-minute NQ chart for ADX regime detection and VWAP slope calculation

- Filter your

OnBarUpdate()logic withBarsInProgresschecks so regime detection runs on the 15-minute data and entries trigger on the 5-minute data

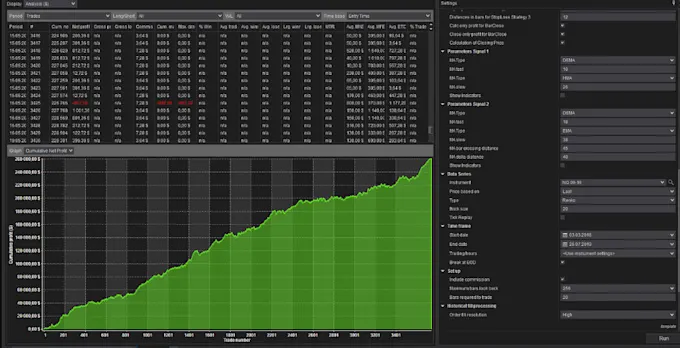

Backtest Reality Check: When It Works and When It Doesn't

Let's talk real numbers. Not cherry-picked trades. Not hypothetical equity curves. The actual performance characteristics of mean reversion on NQ across different conditions.

When Mean Reversion Works

- Range-bound, low-ADX environments: Win rates of 60-68% with average winners roughly equal to average losers. The edge is in the win rate. Typical profit factor: 1.3-1.6.

- Post-trend consolidation: After a multi-day trending move, NQ often enters a 2-5 day consolidation phase. Mean reversion during these periods performs well because the market is genuinely rotating.

- Midday session (11 AM – 2 PM ET): Volatility drops, directional momentum fades, and institutional VWAP algorithms dominate. This is the highest-probability window for mean reversion.

- Non-event days: Days without major economic releases (FOMC, CPI, NFP) or major earnings reports produce cleaner mean reversion setups.

When Mean Reversion Fails

- Trend days: Win rate drops to 25-35%. Average loss is 2-3x average win because the trend just keeps going. One trend day can erase a week of profits. This is the existential risk of mean reversion.

- High-VIX environments (VIX above 25): Elevated implied volatility means larger price swings and wider distributions. The "mean" itself is shifting rapidly, making static reversion levels unreliable. Mean reversion during volatility spikes is gambling.

- Opening 30 minutes: The 9:30-10:00 AM window is dominated by order flow, news reaction, and gap resolution. Mean reversion during this period has significantly lower win rates than during midday.

- Macro event days: FOMC days, CPI releases, employment reports — price moves on new information, not statistical tendencies. Fading a post-FOMC move because "RSI is oversold" is not mean reversion. It's ignorance.

Realistic Expectancy Numbers

If you're doing this right — with regime detection, proper filters, and disciplined stops — here's what realistic mean reversion performance looks like on NQ:

---

Win rate: 58-65%

Avg winner: 15-25 points ($300-$500/contract)

Avg loser: 18-30 points ($360-$600/contract)

Profit factor: 1.2-1.5

Trades per week: 3-8 (highly filtered)

---

Monthly expectancy (1 contract): $800-$2,500

Note: After commissions, slippage. Before tax.

Max drawdown: 4-8% of account (if sized correctly)

Those numbers look modest. They should. Anyone promising you 80% win rates or $10K/month on 1 contract with mean reversion is either lying or curve-fitting. A profit factor of 1.3-1.5 with controlled drawdowns is a genuinely good strategy. It just doesn't make for exciting YouTube thumbnails.

Position Sizing for Mean Reversion

Mean reversion has a unique sizing consideration: because you're fading a move, the trade can go further against you before working. This creates a natural temptation to scale in — adding to a losing position because "it's even more overextended now." This is both the greatest strength and the greatest danger of mean reversion sizing.

Scaling In vs. Full Position

Scaling In (Planned)

Enter with 1/3 of your intended position at the first signal. Add another 1/3 if price extends further with additional confirmation. Add the final 1/3 at the maximum planned extension.

- Better average entry price

- Reduces initial risk exposure

- Requires pre-planned levels and a hard max position size

- Only works if you have a strict stop for the full position

Full Position Entry

Wait for all three confirmations (band touch + RSI extreme + delta divergence) and enter with the full position at once.

- Simpler execution — one entry, one stop, one target

- No temptation to keep adding to a loser

- Fewer trade opportunities (must wait for full confirmation)

- Better for traders who struggle with discipline

The Scaling-In Trap

Scaling in becomes dangerous when it's unplanned. "It dropped another 20 points, I'll add more" is not a strategy — it's averaging down with extra steps. The distinction: planned scaling has predefined entry levels, a maximum position size, and a hard stop for the entire position before the first entry is placed. Unplanned scaling is how accounts die. If you don't have all three elements defined before you trade, use full position entry.

Sizing Formula

Max risk per trade: 1.5% = $1,125

---

Stop distance: 25 points × $20/point = $500/contract

→ Max position: 2 NQ contracts ($1,000 risk)

---

If scaling in 3 tranches:

Entry 1: 1 contract at signal

Entry 2: 1 contract at +10 pts extension

Hard stop for both: 25 pts from Entry 1

Max risk: ~$900 (accounts for averaged entry)

5 Common Mistakes That Destroy Mean Reversion Traders

These aren't hypothetical. These are the patterns we see repeatedly in traders who can't make mean reversion work despite understanding the concept. Knowing the mistake isn't enough — you have to build systems that make the mistake impossible.

Mistake #1: Fading Into Momentum

"NQ is up 150 points, it has to pull back." No, it doesn't. On a genuine trend day, NQ can move 300-500 points with barely a 30-point retracement. Fading a move simply because it "looks extended" without checking regime, volume profile, or VWAP slope is the fastest way to blow up a mean reversion account.

The fix: Never take a mean reversion trade without first confirming the regime filter (ADX below 22, VWAP relatively flat, price has crossed VWAP at least once today). If you can't confirm range conditions, the trade doesn't exist.

Mistake #2: No Regime Filter

Related to #1 but more systemic. Many traders have a mean reversion setup that works beautifully in backtests because the backtest period happened to be range-bound. The moment the market shifts to a trending phase, the same setup hemorrhages money. If your strategy doesn't have an explicit regime gate — a condition that must be true before any trade is considered — your backtest is useless.

The fix: Build the regime filter as the first check in your strategy. If the regime is trending, the strategy does nothing. This feels like "missing trades" and it is — trades you would have lost.

Mistake #3: Sizing Too Big on the First Entry

The first signal in a mean reversion sequence is the lowest-probability entry. Price is overextended, but you don't yet know if it's going to revert or keep extending. Loading up your full position on the first signal means your average entry is at the worst possible price, and your exposure is at maximum when uncertainty is highest.

The fix: If scaling in, start with 1/3 or 1/2 position. If going full position, wait for all three confirmation signals before entering. Either way, your first entry should represent the smallest risk commitment of the trade.

Mistake #4: Ignoring Time of Day

Mean reversion at 9:35 AM and mean reversion at 12:30 PM are completely different trades with completely different win rates. The morning session is momentum-driven — news, gap fills, and aggressive order flow dominate. Fading a morning extension is fading institutional momentum. By contrast, the midday session is naturally rotational, and VWAP-based mean reversion setups have their highest hit rate.

The fix: Restrict mean reversion trades to 10:30 AM – 2:30 PM ET. This eliminates the opening volatility and the closing-hour repositioning, leaving you with the cleanest rotational window. Yes, you'll "miss" morning reversals that would have worked. You'll also miss the morning fakeouts that would have destroyed you.

Mistake #5: No Max Loss for the Day

Mean reversion has a dangerous psychological profile: losses feel "wrong" because the trade thesis is "price is too far from the mean." When a mean reversion trade loses, the temptation is to immediately take another one — because now price is even more extended. This leads to a cascade of losses on trend days where each entry is worse than the last.

The fix: Set a hard daily loss limit — 2% of account or 2 consecutive losing trades, whichever comes first. When you hit it, close the platform. Not "close the chart." Close the platform. Walk away. The market will be there tomorrow.

Frequently Asked Questions

Can I combine mean reversion with breakout strategies?

Yes, and you should. The best NQ traders don't pick one approach — they switch based on regime. Use mean reversion in range-bound conditions and breakout strategies in trending conditions. The regime detection filter is the same for both: it just tells you which playbook to use today. Some automated strategies, including tools from AlgoGemix, handle this regime switching automatically.

What's the minimum account size for mean reversion on NQ?

For a single NQ contract with proper risk management (1-2% risk per trade, 25-30 point stops), you need at least $50,000-$75,000. That's not a regulatory requirement — that's math. A 25-point stop is $500. At 1% risk, that's a $50K account. If that's too large, trade MNQ (Micro NQ) at $2/point, which brings the minimum to $5,000-$7,500 for the same risk percentages. Do not attempt NQ mean reversion with a $10K account. The position sizing doesn't work and one bad day will put you in margin violation.

How many trades per day should a mean reversion strategy produce?

A well-filtered mean reversion strategy on NQ should produce 0-2 trades per day, averaging about 4-8 trades per week. If your strategy is generating 5+ signals daily, your filters are too loose. More signals doesn't mean more profit — it means more noise, more commissions, and more exposure to regime-misidentification risk. The best mean reversion days produce one clean setup with clear confirmation. Many days produce zero setups, and that's correct.

Does mean reversion work on other futures besides NQ?

Mean reversion is a statistical concept that applies to any liquid instrument. ES (S&P 500 futures) has smoother VWAP reversion characteristics than NQ because of lower volatility. Crude oil (CL) and gold (GC) also exhibit strong mean reversion tendencies around VWAP. NQ is unique because its higher volatility creates wider overextensions (bigger entries) but also more violent trend days (bigger risk). The principles in this guide apply broadly, but the specific parameters (ATR multipliers, RSI thresholds, stop distances) need to be calibrated for each instrument's volatility profile.

Should I use limit orders or market orders for mean reversion entries?

Limit orders, almost always. Mean reversion is a counter-trend entry — you're fading the move. Using market orders to chase the entry defeats the purpose. Place a limit order at your desired entry level (e.g., the 2σ VWAP band) and let the market come to you. If it doesn't reach your level, you don't have a trade — and that's fine. The one exception: if you're entering on delta divergence confirmation, a market order is acceptable because you're responding to a real-time order flow signal that won't wait for your limit.

The Bottom Line

Mean reversion on NQ futures is a legitimate edge when applied correctly. The statistical tendency for price to return to a volume-weighted average is real, measurable, and persistent across market cycles. VWAP, the prior day close, and overnight midpoint all act as genuine attractors that institutional algorithms use as execution benchmarks.

But the edge is narrow, and the failure modes are catastrophic. One trend day of unhedged mean reversion trades can erase a month of profits. This isn't a strategy you can learn from a YouTube video and deploy Monday morning. It requires regime detection that actually works, entry filters that eliminate low-conviction setups, stop placement that limits your exposure to tail risk, and the discipline to do nothing on 30-40% of trading days when conditions don't support reversion.

If you build it right — with the triple confirmation entry (Bollinger Bands + RSI + delta divergence), a real regime filter (ADX + VWAP slope), and strict position sizing — you can extract consistent, modest returns from a market that spends most of its time rotating around fair value. The key word is "modest." A profit factor of 1.3-1.5 is genuinely good. It won't make you rich overnight. But it won't blow you up either, which is more than most NQ strategies can claim.

Start on MNQ. Backtest across multiple regimes. Paper trade for at least 4-6 weeks. Track your win rate by time of day and regime type. And when a trend day shows up — and it will — respect your stops and walk away. The mean will be there tomorrow.