Why Backtesting Matters

Backtesting is the process of testing a trading strategy on historical data to see how it would have performed. It's the closest thing to a time machine for traders - allowing you to validate ideas before risking real capital.

Without backtesting, you're essentially gambling. You might think your strategy is brilliant, but the market doesn't care about opinions - it cares about edge. Backtesting provides objective, quantifiable evidence of whether your strategy has that edge.

What Backtesting Reveals

Statistical Edge

Does your strategy actually make money over time? Not just occasionally, but consistently across different market conditions.

Risk Profile

How much can you expect to lose before you win? Maximum drawdown shows your worst-case scenario.

Parameter Sensitivity

How much do results change with small parameter adjustments? Robust strategies work across a range of settings.

Market Condition Fit

When does your strategy shine? When does it struggle? Understanding this helps you know when to trade and when to sit out.

Critical Warning

Backtesting shows how a strategy would have performed, not how it will perform. Past performance doesn't guarantee future results. The goal is to find strategies with a logical, sustainable edge - not to chase historical returns.

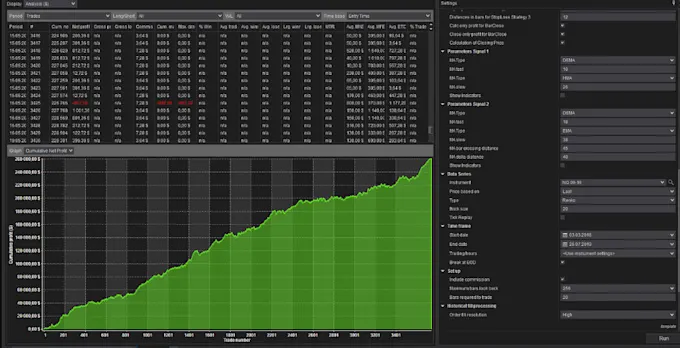

Setting Up Strategy Analyzer in NinjaTrader 8

The Strategy Analyzer is NinjaTrader 8's dedicated backtesting tool. Here's how to use it effectively.

Accessing the Strategy Analyzer

- Open NinjaTrader 8

- Click New in the Control Center

- Select Strategy Analyzer

- Or use keyboard shortcut:

Ctrl+Shift+A

Configuring Your Backtest

- Strategy: Select your strategy from the dropdown. Ensure it's compiled without errors.

- Instrument: Choose the instrument to test (ES, NQ, CL, etc.)

- Data Series: Select timeframe (1 min, 5 min, daily, etc.)

- Date Range: Set start and end dates for the test

- Starting Capital: Your initial account balance for the test

- Commission/Slippage: Include realistic transaction costs

Running the Backtest

Once configured, click Run Backtest. NinjaTrader will process the historical data and generate a detailed performance report.

For grid trading strategies, which operate on ranging markets, you'll want to test across periods that include both trending and ranging conditions to understand how the strategy behaves in each.

Data Requirements

The quality of your backtest is only as good as the quality of your data. Here's what you need to know.

Tick Data vs Minute Bars

| Data Type | Best For | Considerations |

|---|---|---|

| Tick Data | Scalping, HFT, precise entries | Most accurate but requires significant storage; backtests run slower |

| 1-Minute Bars | Day trading, most intraday strategies | Good balance of accuracy and speed; sufficient for most use cases |

| 5-15 Min Bars | Swing strategies, trend following | Faster backtests; may miss intrabar reversals |

| Daily Bars | Position trading, long-term strategies | Longest history available; ignores intraday price action |

Historical Data Sources

- Kinetick (Free): End-of-day data included with NinjaTrader. Good for learning and long-term strategy testing.

- CQG/Rithmic (Paid): Professional-grade historical data with tick-level accuracy. Required for serious intraday backtesting.

- IQFeed: Popular data provider with excellent historical coverage and reliability.

Data Quality Checklist

- No gaps in trading sessions (missing data creates false signals)

- Correct session times for your instrument

- Adjusted for splits and dividends (if applicable)

- Sufficient history (minimum 2-3 years for most strategies)

Key Metrics to Analyze

Understanding these metrics helps you evaluate whether a strategy is worth trading. Don't focus on just one - look at the complete picture.

Primary Performance Metrics

Profit Factor

Gross profit divided by gross loss. Shows how much you make for every dollar you lose.

1.0 - 1.5: Marginal edge

1.5 - 2.0: Good edge

Above 2.0: Excellent (verify not over-optimized)

Maximum Drawdown

The largest peak-to-trough decline during the test period. This is your "pain threshold" metric.

Rule of thumb: Expect live drawdown to be 1.5-2x your backtest drawdown. If you can't stomach 2x the backtest drawdown, reduce position size.

Sharpe Ratio

Risk-adjusted return. Measures excess return per unit of risk.

0.5 - 1.0: Acceptable

Above 1.0: Good

Above 2.0: Excellent

Secondary Metrics

Win Rate

Percentage of winning trades. A 40% win rate can be highly profitable with good risk/reward.

Average Win/Loss Ratio

Average winning trade divided by average losing trade. Higher is better.

Max Consecutive Losses

Longest losing streak. Important for psychological preparation.

Trade Count

Total trades in the test. More trades = more statistical significance.

Skip the Trial and Error

Our professional strategies are rigorously backtested and optimized. Start with proven systems while you develop your own.

Optimization: Finding the Sweet Spot

Optimization tests multiple parameter combinations to find the best performing settings. It's powerful but dangerous when misused.

Walk-Forward Optimization

The gold standard for optimization. Walk-forward testing divides data into "in-sample" periods (for optimization) and "out-of-sample" periods (for validation).

Year 3: Test optimized parameters (out-of-sample)

Year 2-3: Re-optimize

Year 4: Test (out-of-sample)

... and so on

This simulates how you would actually use the strategy: optimize on past data, trade forward, then re-optimize periodically.

Avoiding Curve Fitting

Curve fitting (over-optimization) creates strategies that work perfectly on historical data but fail live. Warning signs:

- Too many parameters: More than 5-6 optimizable parameters is a red flag

- Narrow optimal ranges: If results collapse with small parameter changes, the strategy is fragile

- Unrealistic returns: 500%+ annual returns probably won't persist

- Low trade count: Less than 100 trades doesn't provide statistical significance

Parameter Sensitivity Analysis

Test how your strategy performs across a range of parameter values. A robust strategy should:

- Remain profitable across a wide range of parameter values

- Show gradual performance changes, not cliff edges

- Have the "optimal" values near the center of the profitable range

For example, when testing a grid trading strategy, the grid spacing parameter should work across a range (say 10-25 ticks) not just at exactly 15 ticks.

Common Backtesting Pitfalls

Even experienced traders fall into these traps. Being aware of them is the first step to avoiding them.

Lookahead Bias

Using information that wouldn't have been available at the time of the trade. Examples:

- Using today's close to make decisions during today's session

- Using future earnings announcements to trade before the event

- Referencing indicator values before they've fully calculated

Survivorship Bias

Testing only on instruments that still exist today. Delisted stocks, bankrupt companies, and expired contracts are excluded from current data, making historical returns look better than they were.

Ignoring Transaction Costs

A strategy that makes $50 per trade sounds great until you realize commissions are $4.50 round-trip and slippage costs another $12.50. Always include realistic costs.

Commission: $2.25 per side ($4.50 round trip)

Slippage: 1-2 ticks = $12.50-$25.00

Total per trade: ~$17-$30

Confirmation Bias

Looking for reasons why a strategy should work instead of reasons it might fail. Combat this by:

- Actively trying to break your strategy with adverse conditions

- Having someone else review your logic

- Testing on completely different instruments

The Over-Optimization Warning

If your backtest results seem too good to be true, they probably are. A strategy with 95% win rate and 300% annual returns is almost certainly curve-fitted. Sustainable edges are more modest - expect 55-65% win rates and 20-50% annual returns for robust strategies.

From Backtest to Live: The Reality Gap

Live trading will never exactly match backtest results. Understanding why helps you set realistic expectations.

Why Live Differs from Backtest

Slippage Reality

Backtests assume perfect fills. Live trading faces slippage, especially in fast markets or with larger orders.

Data Differences

Live data feeds may differ from historical data. Small timing differences can affect fill prices.

Market Impact

Your orders affect the market. Backtests ignore this, but larger positions can move prices against you.

Psychology

Real money creates real emotions. You might deviate from the strategy during drawdowns.

Bridging the Gap

- Paper trade first: Run the strategy in simulation with live data to catch issues before going live.

- Start small: Trade minimum position size. Verify results match expectations before scaling.

- Keep a trading journal: Track every trade and compare to what the backtest would have done.

- Be conservative with expectations: Expect 60-80% of backtest performance in live trading.

Strategies like trend following may show better backtest-to-live correlation because they don't require precise timing, while scalping strategies often see larger degradation due to their reliance on exact fills.

Pro Tip

Professional strategies like Grid Pro and Scalper Pro have been tested in live conditions, not just backtests. This real-world validation is worth considering when you're ready to trade live.